European Collateral Management System – A Need for Complete Harmonization in the Pan-Europe Collateral Markets

The European Collateral Management System (ECMS) is a harmonized and integrated system with the vision of organizing a single platform for collateral services across Europe through Target 2 Securities (T2S). T2S is a revolutionary security settlement platform that provides access to centralized infrastructure to entire market participants in the post-trade landscape. Development and testing of T2S are currently ongoing across Europe at a high phase. ECMS is one of the key components of T2S, and there is a strict timeline for ECMS participants to enable required functionalities and messaging standard migration to avail of harmonized ECMS services. Market participants are working towards technical configurations and business processes considering the ECMS go-live date of November 2023.

What is ECMS and how does it benefit from the existing local collateral management systems (CMSs)?

European Central Bank’s (ECB) Eurosystem Collateral Management System is implemented by 19 national central banks across Europe. This project consolidates Eurosystem market integration and harmonization initiatives, which aim to develop a standard platform and systems that work across Europe.

Benefits

- Single collateral systems for Eurosystem credit operations with closer integration of security and cash operations

- Counterparty will now not have to interact with different local collateral systems

- Harmonized collateral management and billing processes

- Increased re-use of solutions across triparty agents

- Harmonized CA events across Europe, exercise of shareholder rights, and decommissioning the legacy systems

- ECMS supports settlement of marketable assets and auto-collateralizations

- ECMS is based on ISO 20022 message standard for increased functionalities

- It allows the repurposing of excess collateral to automatically increase the credit line and automatically handle corporate actions (CA) pertaining to eligible marketable assets.

- Single system for managing a range of assets that are used as collateral within the Eurosystem credit operation

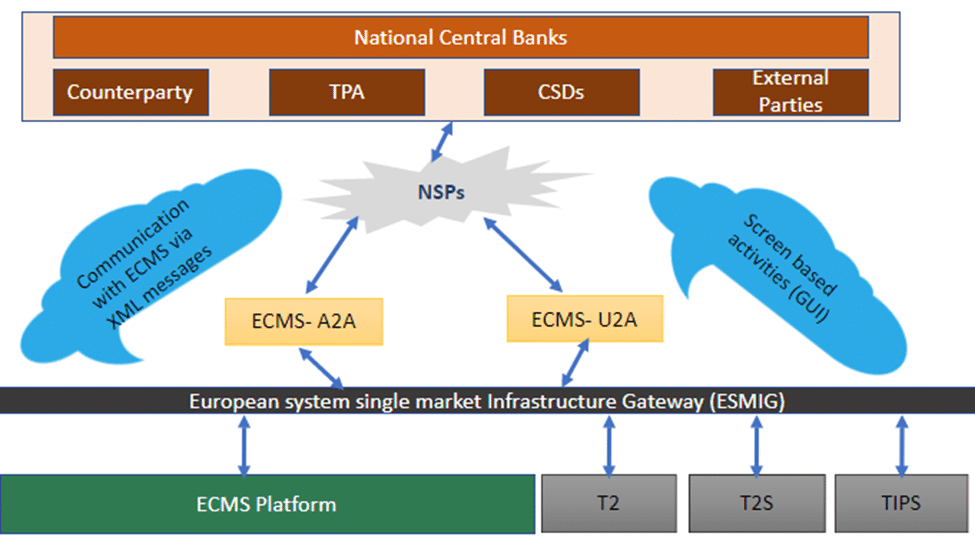

Who are the participants to interact with ECMS and what are its core functions?

Participants who connect and interact with ECMS regarding collateral services are counterparties, triparty agents, and central security depositories; they communicate using two different modes: application to application (A2A) and user to application (U2A).

Below are the key functions of ECMS participants.

Figure 1: ECMS – ECMS Participants connectivity through ESMIG

Counterparties: Counterparties normally refer to brokers, dealers, investment banks, and other security dealers; this acts as an entity that participates in the payment or security transaction of ECMS. Below are the core functions of counterparties:

- Security settlement

- Payments Clearing and Settlements

- Cash management and collateral management

Entities that act as counterparties are European Central Counterparty N.V., Eurex Clearing AG, Cassa di Compensazione e Garanzia S.p.A. (CCG), European Commodity Clearing, and ICE Clear Netherlands B.V.

Central security depositories: CSDs are the financial institutions holding securities and take care of complete billing, corporate actions, and asset services.

- Administration of corporate actions and redemption

- Security services and safekeeping

- Legal transfer ownership and custody services

- Billing instructions for mobilizations

Firms that operate as CSDs are Euroclear, CEDEL GROUP, Finnish Central Securities Depository Limited, and Deutscher Kassenverein AG.

Triparty Agents: Triparty Agents offers triparty collateral management services that allow market participants to take advantage of collateral availability through different markets. Some of the core functions are listed below:

- Collateral management functions

- Triparty transaction amount handling

- Reference data management

- Billing instructions for mobilizations

- Corporate action functions

Firms that operate as Triparty Agents are Clearstream Bank Luxembourg, Euroclear Bank, Bank of New York Mellon, JP Morgan, and SIS.

Key harmonization activities of the ECMS

Below are the harmonization activities that have been identified by the stakeholders; each activity has several business processes and workflows.

Triparty collateral management- Harmonization of collateral management workflows and messaging in-order to facilitate interoperable processes allowing collateral mobility across triparty agents

Corporate actions- Harmonization of corporate actions processes, workflows, and messaging by reinforcing existing standards or adding new harmonization standards

Taxation processes- Taxation processes, in the context of collateral management, account identification of parties in collateralized transactions

Bilateral collateral management- Interoperability and leverage to existing infrastructures and market platforms

Margin calls- A need for harmonization has been identified for the wider use of electronic platforms for margin calls

Billing processes- Holding collateral in different CSDs involves subsequent requirements on the collateral givers and takers in terms of adhering to different CSD processes, reconciliation, and payment of fee invoices (collaterals)

Cut-off times- Mobilization of collaterals between delivery versus payment (DVP) and free of payment (FOP)

Collateral dynamic and static data- Ensures the core collateral data needs to be exchanged in a timely manner.

Sourcing of collateral- Timely sourcing of collateral is fundamental to the efficient functioning of collateral management processes. Time taken to process collateral instructions and further improve settlement processes. The market is also considering encouraging non-T2S CSDs to join T2S, which would aid in the market’s achievement of the level of service.

Non-Euro collateral- Harmonization is required in the sourcing of non-euro-denominated collateral as well as the handling of cash flows resulting from CA events involving non-euro-denominated assets.

Issue and Barriers to effective and efficient collateral management systems

The transition from current disparate manual processes and content to ISO-based standardized messaging and workflows will need elaborate electronic mechanisms and will likely add a significant burden on all financial intermediaries involved, i.e., the CSDs, TPAs, and custodians.

Some of the common issues faced by ECMS participants are:

- Local collateral arrangements resulting in fragmentation that requires market participants and their Eurosystem counterparties to go through different procedures to deal with mobilizing collateral.

- Difference in procedures lead to operational inefficiencies that can be detrimental in times of financial stress and collateral shortages, which result in unnecessary cost.

- Existing collateral arrangements leave the door open for differences in business processes and messaging for cross-border collateral management activities that lead to operational impediments involving triparty and collateral management arrangements.

- Handling of corporate actions and taxations with the involvement of agents (TPAs and CSDs) when securities are used as collateral.

- Barriers to post-trade arrangements in European financial markets that include legal and regulatory barriers

- One of the major challenges is the adoption of ISO 20022. Participants have incorporated the ISO 15022 standard for its efficiency, automation, and benefits over the years. However, many firms struggle with financial incentives to switch to ISO 20022.

Migration and Testing Approach- Stakeholders involvement and responsibilities

The ECMS migration process is expected to be aligned with its mandate from the two working groups, the User Testing and Migration Subgroup (UTMSG) and the ECMS Working Group (ECMS-WG). This defines the strategy to smoothen the transition of the current collateral management system to the new ECMS.

NCBs to move all the current collateral management functionalities from existing local collateral management (CMS) systems to new systems.

ECMS migrations will be a big-bang approach, where all respective participants, such as national central banks and their communities (CPTYs, CSDs, and Triparty Agents), will be migrated simultaneously.

Stakeholders’ participation in terms of migrations and testing – below are the entities who are required to perform the extensive testing of the ECMS migration.

- ECB- European Central Bank

- NCB- National Central Bank

- T2 and T2S service desk and ECMS service desk

- CPTYs- Counterparties

- CSD- Central securities and depositories

- TPAs- Triparty Agents

- NSPs- Network service providers

Testing Approach- Plan, Phases, and Environments

Testing period is planned to have two different stages and will be performed in two testing environments – The Interoperability test environment and Pre-production environment.

Test stages: – 1) Eurosystem Acceptance Testing Stage (EAT) 2) User Testing,

Here are the details of different stages.

- EAT- The testing scope of EAT is high-level functional testing, and European System of Central Banks (ESCB) services will be connected during EAT phase 1.

- Central Bank Testing- High-level functional scope of the central bank testing phase; all ESCB services and the ECMS DWH will be connected in this phase.

- Community Testing Phase1- Community testing phase 1 will have all the parties’, excluding counterparties and non-euro CBs.

- Community Testing Phase 2/Business testing/Operating testing – This phase aims to test the entire functional scope of the ECMS.

Conclusion

It is quite evident that integration and harmonization initiatives bring more efficient collateral management services to pan-European market participants. Essentially, the participants are required to ensure system and connectivity readiness to perform respective ECMS operations.

Cigniti offers comprehensive testing capabilities that are future-proof, including integration testing, API and component-level testing, functional and non-functional testing, and so on.

Cigniti offers solutions to the ECMS standard requirement, such as quality assurance, migrations, ISO 20022 conversions, validations, etc. It also ensures the testing frameworks and SWIFT test artifacts are in line with the Eurosystems standard guidelines and practices. Cigniti would extend support to ECMS players on all the test cases that are executed as mentioned in the European Central Bank (testing artifacts) repository.

Need more help? Talk to our BFSI experts to understand more details about Target Services and Collateral Management Services.

Leave a Reply