Fraud Detection in Insurance Claim Process by Using Artificial Intelligence

Fraudulent insurance claims are one of the biggest preventable losses that hurt insurers worldwide. The P&C segment accounts for the most fraudulent insurance claims, with auto insurance and workers’ compensation making up the biggest percentage of fraudulent claims that annually impact the insurance business.

Traditionally, insurers have detected fraud manually. Due to the inherent drawbacks of these techniques, undetected fraud continues to put a strain on insurers. Since this method relies on existing fraud data, new frauds could also easily go unnoticed. Some fraudulent claims sneak through the system when just sampling methods are employed to analyze claims for fraud. In addition, the old approach is not designed to handle the influx of data and information from numerous new and various sources of information in an integrated way because it only functions in silos.

What is Insurance Fraud?

When an insurance firm, agent, adjuster, or customer intentionally lies to get an unfair advantage, then insurance fraud occurs. It can happen when purchasing, utilizing, reselling, or underwriting insurance. Insurance fraud can be classified into various subcategories, including fraud committed by consumers and insurance firms. Fraud affects consumers and businesses financially, in addition to adding to insurance companies’ costs.

All insurance industries, including medical, auto, and home insurance, are rife with fraud. Even today’s most well-known insurance firms understand that insurance fraud occurs, they sometimes lack the resources to identify and look into all possibly fraudulent claims.

Claim fraud is the most common sort of insurance fraud out of all the different kinds. Organizations that manually file claims are frequently left unequipped as fraudsters’ tactics become more complex and firms lack the technical capacity to keep up, whether it be an individual making an overstated claim or a coordinated conspiracy among many to exploit insurance companies. Insurance claim fraud is not recent, but it has always proven challenging to eradicate.

Insurance Fraud Types

Here are two major insurance fraud types:

i) Hard fraud is the act of deliberately faking injury or damage to get money from an insurance company.

ii) Soft fraud involves exaggerating the damage caused by a real accident to get more money from the claim.

More specifically, these are some of the most common insurance fraud types split by niche:

Workers’ Compensation Benefit fraud: Fakes an injury at work to get paid time off, claims an injury occurred on the job when it took place elsewhere, etc.

Property insurance fraud: False or inflated property damage, false or inflated burglary or theft report, arson, intentional damage claim, etc.

Auto insurance fraud: False repair claim, staged accident, intentional damage claim, auto shop scam, falsifying the date or details of an accident, etc.

Disability and healthcare fraud: Includes billing for services that were not provided, falsifying documents to bill for a more expensive service than what was actually provided, falsifying documents to obtain and bill for unnecessary services, double billing, falsifying disability claims, submitting forged documents to continue a disability claim, and so on.

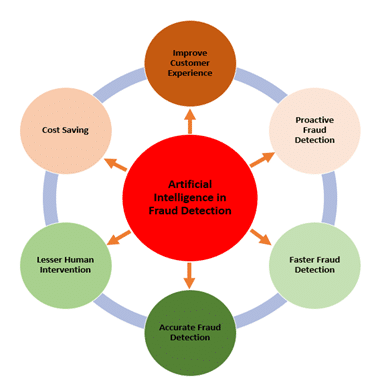

Benefits of Insurance Fraud Detection by using AI

1. Proactive fraud detection

Predictive analytics brings more opportunities to conduct proactive fraud detection initiatives. Today’s organized, digital frauds require advanced, data mining, analytics, and customized fraudster behavioral pattern-based algorithms to be programmed for proactive, timely scam detection.

The technology identifies the root causes of fraudulent activities and uses the data to foresee fraud and combat it proactively.

2. Faster fraud detection

AI technology not only automates the fraud detection process but also identifies fraud patterns, allowing early flagging and prompt response to any potential incidents.

As the number of clients increases, claims adjusters are put under more pressure and should either sacrifice accuracy or speed in the claims process. On the contrary, the more data machine learning algorithms receive, the faster they provide accurate results.

3. Accurate fraud detection

Next, predictive analytics delivers way more accurate results than a human agent can do. As a result of processing big data, digital tools have more information to make decisions with never before seen accuracy.

4. Lesser human interventions

By maximizing the use of technology and data analytics, insurers reduce the number of manual interventions in the claim management process. This reduces turnaround times and frees up insurance agents, allowing them to focus on more valuable, high-impact tasks.

5. Cost savings

With more accurate fraud detection and fewer false positives made possible by AI technologies, insurers can significantly decrease financial loss. Also, by automating repetitive processes like fraud detection, you won’t need to increase your headcount as you scale up – which otherwise would have come with extra costs.

6. Improved customer experience

All things considered, automated insurance fraud detection powered by AI and big data allows insurers to reduce costs and offer more competitive insurance plans to customers.

Leveraging Artificial Intelligence for Insurance Claim Fraud detection

One of the top priorities for insurers when it comes to insurance claims is identifying and stopping the payment of fraudulent claims as quickly and effectively as possible. The reduction of client premium costs can result from preventing fraudulent claims, which benefits an insurance company’s bottom line and performance. AI has the potential to change this situation. Information systems have undergone significant change thanks to AI technologies, which have made them more user-friendly and straightforward.

The use of AI in claims fraud detection is quite helpful, increasing client happiness and sparing businesses money.

In the millions of insurance claims that businesses receive each year, machine learning and AI algorithms can quickly identify patterns, enabling them to spot outliers and dubious requests in real time.

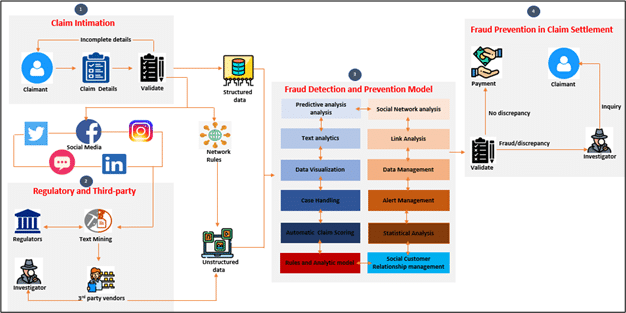

Claim Fraud detection and prevention model

Predictive Analytics for Insurance Fraud Prevention:

Predictive analytics for early identification and fraud prevention is the first line of defense against fraudulent insurance claims. Predictive analytics may evaluate the policyholder’s fraud risk and offer an early warning for possibly fraudulent activities based on their profile and behavior patterns with each new customer touchpoint and more information collected.

When using AI for claim fraud detection, the algorithms accurately assess each claim and provide a reason code, which can help identify whether the request is suspicious and needs to be looked into further. Insurance companies can better allocate resources to investigate claims that have been detected as possibly fraudulent and save time and money by warning personnel about potentially fraudulent claims before processing and pay-outs.

Use of Predictive analytics in Claim, Pricing and New Product design:

Fraud prevention helps insurers prevent fraud at different levels of the insurance cycle, including applications, premiums, claims, etc. It provides access to public records such as criminal records, medical histories, and bankruptcy declarations to review data for inconsistencies and fraud prevention.

Pricing and risk mitigation – Offer insights that facilitate decision-making and estimate the level of risk that the insurance company must assume while calculating the premium. For instance, those who go to the gym regularly may be eligible for a discount on health insurance.

Trends tracking – Helps insurers create new products, design new customer experiences, and deploy new technologies by monitoring what’s trending in the insurance world. This also gives insurance companies a competitive edge.

1. Text Analytics and Data Mining:

With these cutting-edge capabilities, AI is assisting in streamlining the complete insurance claims process and assisting businesses in accessing more intelligent fraud detection without the need for additional staff or expenditures. Utilizing AI for claims fraud detection enables businesses to quickly evaluate structured and unstructured data from internal and external sources, improving analytics and enhancing firm protection. The more policyholder data that can be accessed and analyzed, the better organizations can assess the likelihood of fraudulent insurance claims.

Data from insurance applications or claim forms may be mined by insurance companies with the aid of AI. Insurance adjusters typically examine property damage or personal injury claims to assess the reimbursement to policyholders. These adjusters frequently take notes during their assessments. These remarks are frequently handwritten, so they aren’t organized. By looking for red flags in adjuster notes, natural language processing (NLP) could assist insurers in spotting claims that may be fraudulent.

2. Real-Time Monitoring and Notification:

The capacity to analyze data fast and in real-time is one of the biggest USPs of insurance fraud detection utilizing machine learning and artificial intelligence. As a result, insurance companies invest more time avoiding fraud than recovering from it. Businesses can react promptly to occurrences and minimize any losses thanks to real-time event flagging and reporting.

The routines and behaviors of claimants and policyholders are continuously monitored by AI systems. The algorithms can instantly spot potentially fraudulent behavior and immediately notify the business when a claim requires further examination.

Insurance companies can use AI to better defend themselves from claims fraud and related losses by utilizing NLP to evaluate historical claims data, enhanced data mining, real-time alerts, and better early fraud risk detection.

Conclusion

Insurance fraud puts insurance firms at grave financial risk. Thus, they should take proactive steps to improve their fraud protection techniques. Predictive analytics, AI, and machine learning are currently being rapidly embraced in the insurance sector, aiding insurers in their whole business transformation. Artificial intelligence will go a long way toward making the insurance claim settlement process less laborious and more interactive. Additionally, automating the insurance claims process frees up human resources that may be used for tasks other than reading through paperwork. Because these new technologies help insurance companies stop fraud leaks in the claims area, they provide a significant return on investment in fraud analytics.

Cigniti supports global insurers in their digital transformation journey and helps them deliver an improved customer experience and gain a competitive advantage. Our customized services in insurance testing range across Life Insurance (Life, Annuity, and Pension), Property & Casualty (P&C), Auto, and Reinsurance segments.

We ensure your apps and systems run seamlessly by ensuring efficient back-office operations. Our testing services portfolio and matchless track record prove us as a trusted advisor and preferred technology partner for insurance clients.

Leave a Reply